Can you finance a unique property in France as a Scandinavian in 2026? One Danish family's story

Can you get a mortgage in France while living in Norway, Denmark, or Sweden? Is it really possible to buy a property or even a historic mansion in the south of France, when you're a non-resident?

The answer is yes. Every year, Scandinavian families make their dream of owning a home in France come true. And yet, between the cultural differences, the demands of French banks, and the maze of French administration, many give up before they've even begun.

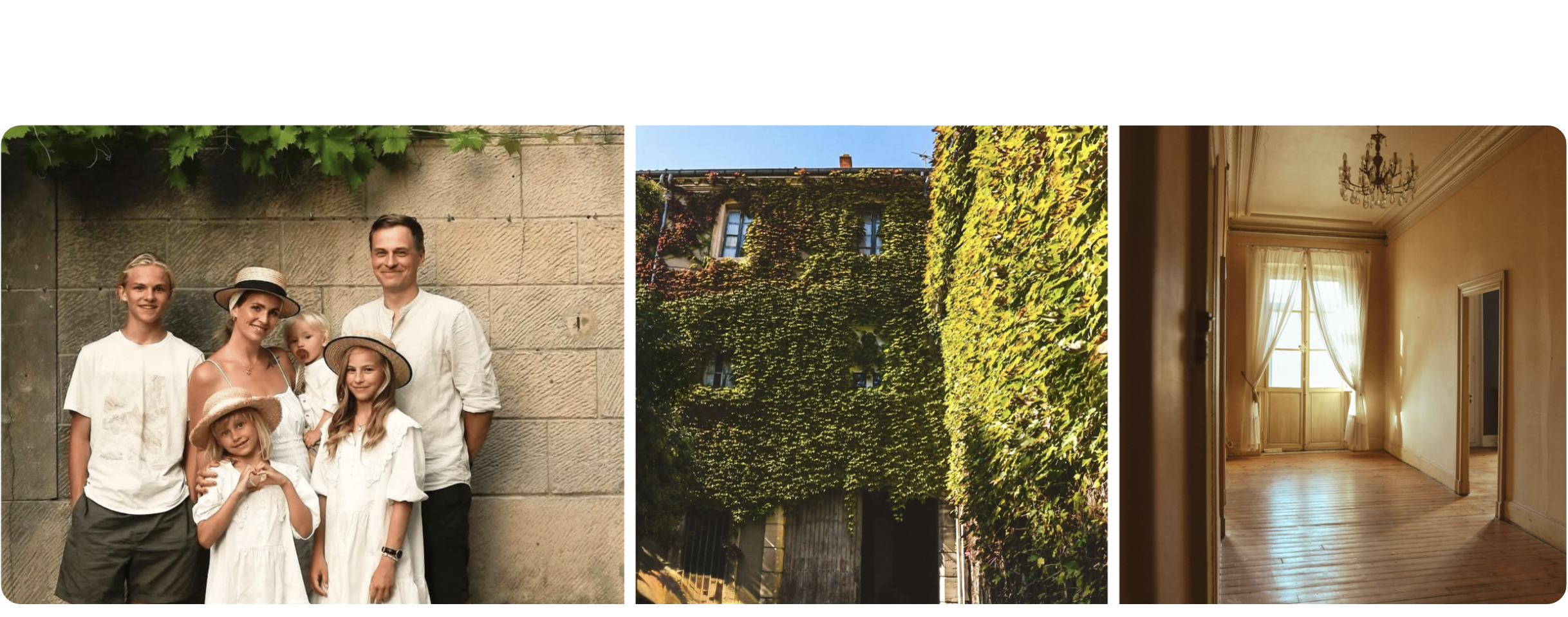

The story of Cornelia and Oliver Nørregaard proves it doesn't have to be that way.

Norwegian-born entrepreneurs and parents of four, they chose to leave a comfortable life behind and settle in the Toulouse region for their first French renovation. They then set their sights on something far more ambitious: restoring a historic mansion in the south of France and turning it into a place that was entirely their own.

They started out as non-residents and later became tax residents: this is the story of a family that managed to turn its dream into reality, despite numerous obstacles, from cultural differences to the challenges of financing a real estate project in France as foreigners.

For any Norwegian, Danish, or Swedish thinking about buying a place in France, their journey holds one essential lesson: the hardest part is rarely finding the right property. It's fitting into those famous "French boxes," the ones that reassure banks, the ones that open every door.

Why are so many Scandinavians choosing the south of France today?

For several years now, France has drawn a growing number of buyers from Norway, Denmark, and Sweden. While one might assume it’s about the weather, the underlying reality is that it’s a search for balance. A gentler pace of life, extraordinary food, and a deep sense of heritage all help explain the pull.

For Cornelia, it started when she was nine. On her first holiday in France, she felt something she couldn't quite put into words: a sense of being exactly where she belonged. She remembers asking her parents, "Why don't we live here?"

Years later, back in the south of France with her husband and children, her own daughter asked her the very same question. And in that moment, everything fell into place. The dream had never gone away, it had simply been waiting for its moment.

Three years later, after a long search, the family fell in love with a first house to renovate near Toulouse. They restored it, sold it successfully, and then decided to find something bolder: a historic mansion in the Languedoc-Roussillon region, to transform into a one-of-a-kind place.

Buying in France as a non-resident: what surprises Scandinavians most?

Ask Cornelia what struck her most when she arrived in France, and her answer comes without hesitation: "How rigid the system is, and how much it costs. It's very, very expensive to live by the rules. In France, you stack up insurance policies and layers of legal protection. For Scandinavians, who are used to trusting people and going with their gut, all that paperwork feels like a wall at first."

For many Nordic buyers accustomed to simpler processes, this can be genuinely disorienting. Cornelia sums up the culture shock perfectly: "These French boxes are so hard for us Scandinavians to understand, because we believe in people, not just numbers. The opposite of fear is trust."

And yet, looking back, she sees the value in it too. Behind the formalities lies a kind of security; behind the caution of the banks lies the need for everyone to be protected.

Can you get a French mortgage while living in Norway, Denmark, or Sweden?

Yes. And contrary to a very common assumption, French banks still finance non-resident buyers in 2026.

That said, the criteria are stricter than they are for a French resident. Banks pay particular attention to:

- your country of residence;

- the stability of your employment;

- the nature of your income;

- the currency your income is paid in;

- the amount of savings you have available;

- your track record as a property owner and investor.

In most cases, a down payment of between 20% and 40% is required.

Some banks may also ask for additional reserve savings, or apply a rate slightly higher than the one offered to residents.

But that's not where the real challenge lies. The truth is, only a minority of banks will actually finance non-residents. In other words, having an excellent application isn't always enough, you need to bring it to the right bank.

Why a broker who specializes in non-residents often makes all the difference

While searching for a property to renovate in the Languedoc-Roussillon region, after countless viewings, dashed hopes, and closed doors, the turning point was finding someone to see the vision through their eyes.

"The biggest tears I cried in this country came from trying, as a Scandinavian, to say who I am, to prove what I can do and what I'm capable of. For a long time I felt unseen, as if my worth just didn't fit into those famous right boxes. Until the day Paul, our broker, asked me the simplest question: tell me about yourself."

She explains: “It was the first time in years that someone had taken an interest in who I really was and asked me why I was doing this project: this enormous house, with its daunting numbers, was actually an excellent idea, because it was part of our entire history.”

That's exactly the role of a financing specialist for expats and non-residents. The job isn't only to negotiate a rate. It's to understand the story behind the numbers, and to translate that story into a language French banks can understand.

IFor the Nørregaards, that approach changed the course of the entire project. As Cornelia puts it: "He believed in us before the banks did."

Why invest in a historic mansion in the south of France?

Today, the once-abandoned building is coming back to life. Noble materials, lime plaster, old hardwood floors, are gradually revealing the property's exceptional potential.

But for the Nørregaards, the goal was never purely financial.

They want to create a place that tells a story, a place to host brands and their photoshoots, events, and one-of-a-kind experiences. In short, a place with a soul.

As Cornelia says: "It's better to build something you truly love than to own something perfectly sensible that makes you feel nothing."

Buying in France as a Scandinavian: Cornelia's advice

If Cornelia had to give just one piece of advice to the Norwegian, Danish, and Swedish families who dream of putting down roots in France, it would be simple: don't wait for the perfect moment, because the perfect moment never comes. The projects that change a life often begin with a single decision: the decision to try.

And when you ask her to sum up the whole adventure in five words, she laughs and says:

"Call Paul and do it."

Follow Cornelia's adventures on her Instagram: French Feelings

Frequently Asked Questions

What down payment is required to purchase real estate in France when you live in Norway, Denmark, or Sweden?

In 2026, French banks generally require a non-resident buyer to make a down payment of between 20% and 40% of the property's price, compared to around 10% for a resident (which mainly covers closing costs). Buyers based in the European Union or the EEA, which includes Sweden, Denmark, and Norway, tend to fall toward the lower end of this range. The exact amount depends on the bank, the stability of the buyer's income, and the overall strength of the application. Some banks also require a contingency savings account.

Do French banks accept income received in kroner (NOK, DKK, SEK)?

Yes, but this is a major point of attention, as Norway, Denmark, and Sweden are outside the eurozone. When paired with a loan denominated in euros, income in kroner creates a foreign exchange risk that French banks hedge by applying a a cut of 10% to 30% to the income taken into account. Some banks even reject applications involving currencies deemed too volatile. The currency in which income is received is therefore one of the factors explaining why only a minority of banks actually provide financing to non-residents. A few institutions offer currency hedging solutions, for example, to lock in an exchange rate between the loan offer and the disbursement of funds.

Do you have to be a French tax resident to buy property in France?

No. Owning real estate in France is not restricted to residents: you can buy and finance a property while remaining a tax resident of your country of origin. Many Scandinavian families start out as non-residents and then become French tax residents once they've settled in, as illustrated by the Nørregaard family's story. Your tax status, however, does affect taxation: rental income from French sources is taxable in France (with a minimum tax rate for non-residents), and the rules depend on the tax treaty between France and each Nordic country. It is recommend to you check your specific situation with a tax advisor, as these treaties vary from country to country.

Why use a broker specializing in non-residents rather than contacting a French bank directly?

Because the main obstacle isn't the quality of the application, but access to the right banks. In 2026, only a minority of French financial institutions provide financing to non-residents, and each has its own criteria regarding country of residence, currency of income, and down payment. Non-residents also face interest rates that are 0.10 to 0.40 points higher than those for residents, a difference that can vary significantly depending on the choice of bank. A broker specializing in financing for expatriates and non-residents knows which bank to approach for each specific profile and translates the story behind the numbers into a language that French banks understand, which can make the difference between rejection and approval.

Updated on June 29, 2026, by Elise Desjardins, Content Specialist for Mortgage Lending & International Financing.

For three years at Pretto Galaxie, one of France’s leading networks of independent mortgage brokers, Elise Desjardins worked at the heart of the French mortgage ecosystem, alongside more than 300 mortgage professionals. There, she developed in-depth knowledge of banking regulations, loan approval criteria, and the practical challenges faced by borrowers. She now writes guides for Opeongo Finance aimed at international clients: Scandinavian, American, and British buyers, French expatriates, and foreign investors who wish to finance a property in France from abroad.